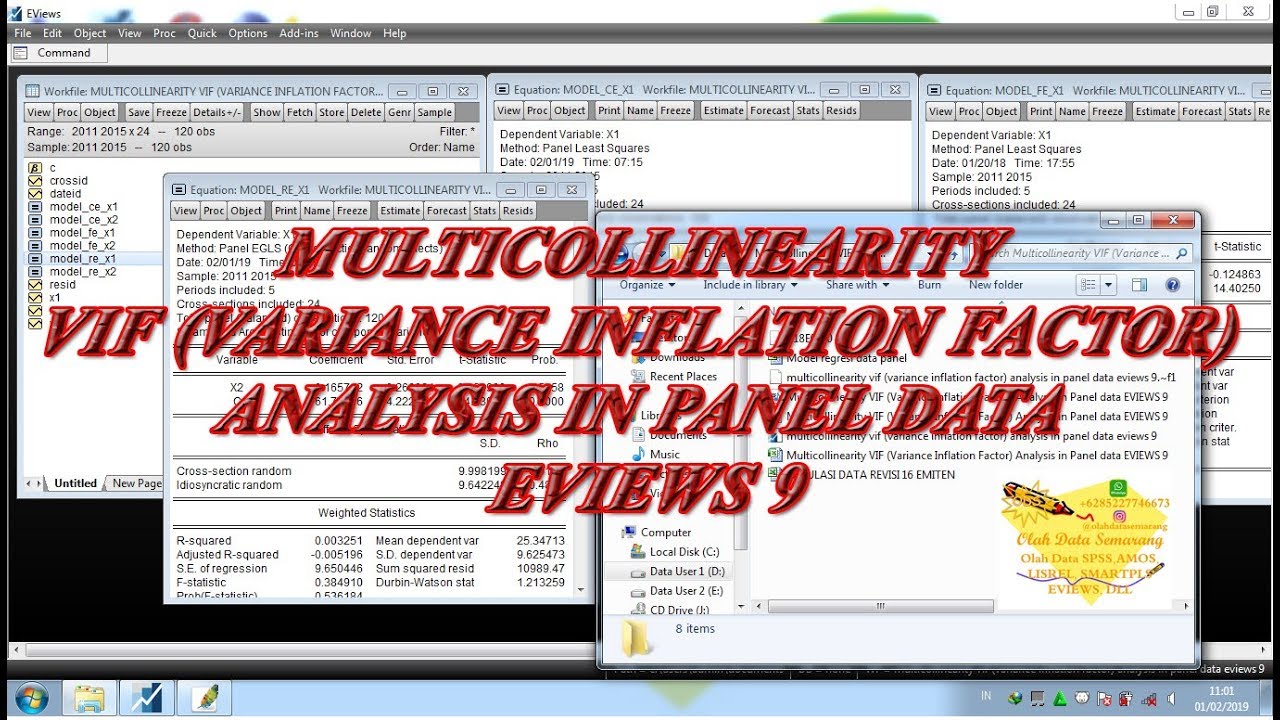

Select the two independent variables x2 and x3 from foreign data source excel file and open it as a group. How do you test for multicollinearity eviews? This is the analysis for multicollinearity vif (variance inflation factor) analysis in panel data eviews 9 with common effect model (cem), fixed effect model.

9 Eviews Output for Volatility Spillover Test Download Table

Parameter estimates drastically change values and become statistically significant when excluding some independent variables from the regression 9.

Dua metode yang mungkin dipakai dalam eviews untuk menilai multikolinearitas pada model regresi terbentuk adalah dengan menilai nilai korelasi antar.

How to solve multicollinearity in eviews? Review scatterplot and correlation matrices. Eviews reports two test statistics from this test regression. 보시면 각 기울기 계수의 t 통계량이 유의함에 따라 그에 상응하는.

The end objective) that is measured in mathematical or statistical or financial modeling.

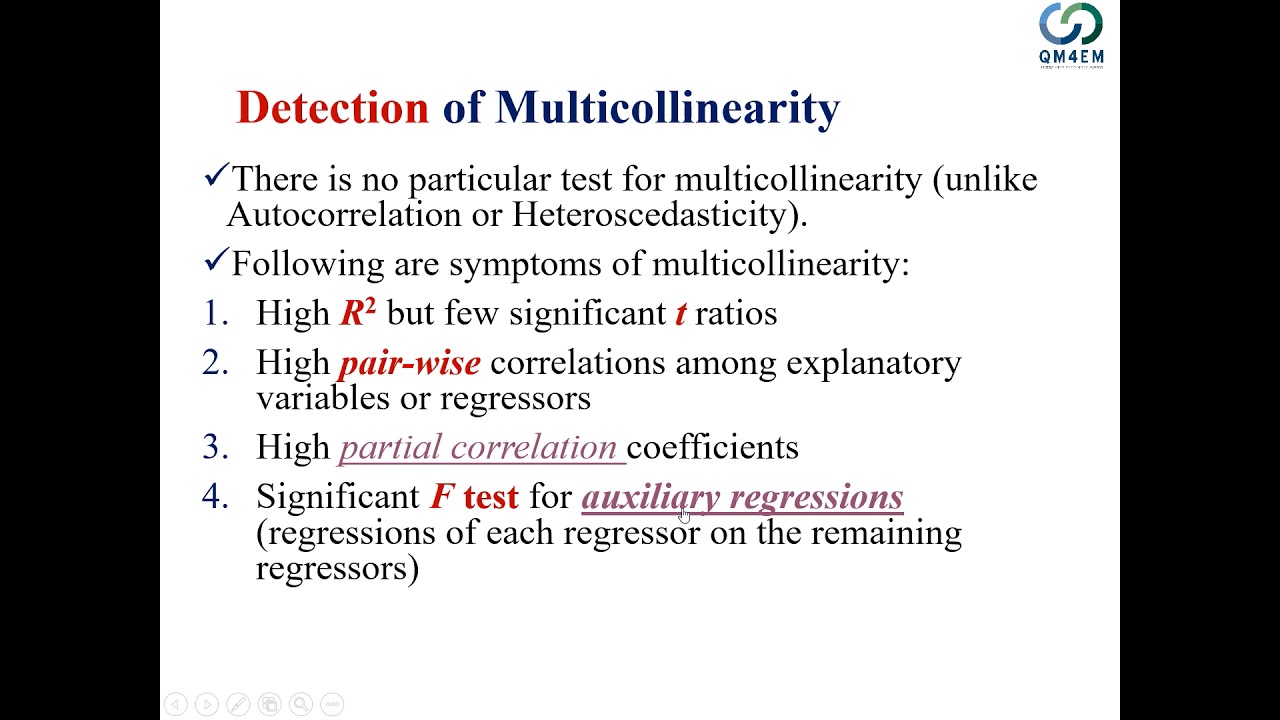

How do you detect multicollinearity in a correlation matrix? Dalam eviews tidak terdapat menu analisis yang menyediakan secara khusus untuk menguji multikolinearitas pada model regresi terbentuk (tidak seperti pada spss dimana terdapat nilai tolerance dan vif). Lalu akan muncul tampilan equation estimator => specification. Ubah persamaan regresi y x c menjadi y c x.

And it is certainly true that a high correlation between two predictors is an indicator of multicollinearity.

A fitness goods manufacturer has created a new product and has done a market test of it in four select markets. 그러면 이제 『eviews 18』 포스팅 때부터 썼던 mlrm 워크파일의 다중 회귀모형으로 다중공선성이 존재하는지 확인해 보겠습니다. But, i did not find any option to test multicollinearity with panel data regression. This correlation is a problem because independent variables should be independent.if the degree of correlation between variables is high enough, it can cause problems when you fit the model and interpret the results.

Third, while there are only two variables here, in the general case of more than 2 rhs variables looking at simple correlations is not an appropriate check for multicollinearity.

Longley.wf1” contains macro economic variables for the us between 1947 and 1962, and is often used as an example of multicollinearity in a data set. This is how you do it: If your goal is to perform the predictions and not necessary to understand the significance of the independent variable, it is not a mandate to fix the multicollinearity issue. Eq_mlrm 방정식을 열어보시면 아래와 같습니다.

But there are two problems with treating this rule of thumb as a rule.

Read more in the equation predict the perfect linear relationship. On the 99% level, you reject the null hypothesis (of homoskedasticity) and there is reason to believe your data suffers from heteroskedasticity to an extent which is a problem. First, if you must check for multicollinearity use the eviews tools that trubador describes. Applications with eviews (cont.) 53 when we drop both the general price level and the price of cars, the multicollinearity problem is solved but r2 is low.

Uji normalitas residual dengan eviews kesimpulan hasil uji multikolinearitas menunjukkan tidak terdapat nilai korelasi yang tinggi antar variabel bebas tidak melebihi 0,90 (ghozali, 2013:83) sehingga disimpulkan tidak.

So we check the second highest correlation between disposable income and price level. You will get a correltion matrix. If it’s above.8 (or.7 or.9 or some other high number), the rule of thumb says you have multicollinearity. When you perform a wald test, eviews provides a table of output showing the numeric values associated with the test.

Pilih proc => make equation.

Results should be less than 1 diagonally for no multicollinearity. However, for time series data, i am finding the option to test multicollinearity. The equation we estimate regresses employment on year (year), the gnp. Multicollinearity occurs when independent variables in a regression model are correlated.